You just made a big sale: a container of your hottest items, headed straight for a new market overseas. You’re picturing the profit, doing the mental math. Then the money hits your account, and it’s… less. Significantly less. Your bank statement looks like a black hole swallowed part of your earnings. Sound familiar?

Welcome to the brutal reality of cross-border transactions. It’s not just about the goods moving; it’s about your hard-earned cash moving too, and every step of that journey is a chance for someone to quietly pick your pocket with ‘fees’ you never saw coming. This isn’t some textbook theory; this is the street-level truth from the operations team at Vantage Forwarding’s Guangzhou Baiyun hub. We see the headaches, the lost profits, and the sheer frustration daily. We’re here to cut through the BS and show you the best payment facilitators cross border transactions 2026 has to offer, without the fluff.

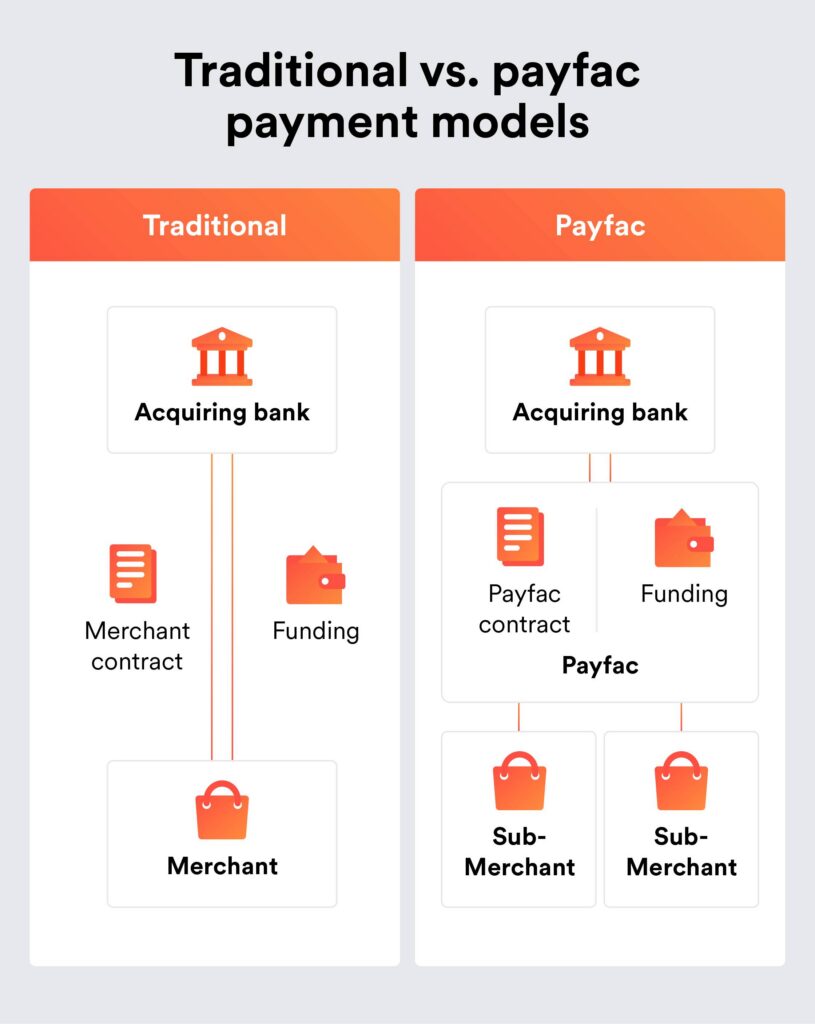

What are these payment facilitators, and why can’t I just use my local bank?

Think of a cross-border payment facilitator as your money’s personal express lane across international borders. Instead of your money taking the scenic, often expensive, route through multiple correspondent banks (each taking a cut), these facilitators offer a more direct, often cheaper, path.

- Your local bank: Great for local stuff. Send money to your supplier down the street? No problem. Send money to a supplier in Vietnam or collect from a customer in Germany? They’ll do it, but they’ll use the SWIFT network, which is old, slow, and expensive. You’ll get hit with wire transfer fees, intermediary bank fees, and often terrible exchange rates.

- Payment facilitators: These guys specialize in moving money internationally. They have networks, local bank accounts in various countries, and technology that streamlines the process. This means faster transfers, often better exchange rates, and clearer fee structures (if you know where to look). They’re essential for e-commerce sellers dealing with international customers or suppliers, because every penny saved on a transaction is a penny in your pocket.

What’s the real cost? Unmasking hidden cross-border fees.

This is where most businesses get burned. The advertised fee is just the tip of the iceberg. You need to understand the whole damn ice field.

Transaction Fees (The Obvious One)

This is usually a percentage of the transaction value plus a small fixed fee. For example, 2.9% + $0.30. It’s upfront, but it adds up.

- Typical Range: 1.5% – 4.5% + $0.20 – $0.50 per transaction

Currency Conversion/FX Fees (The Sneaky One)

This is the biggest rip-off. When you convert USD to EUR or CNY to USD, the facilitator doesn’t give you the ‘mid-market rate’ you see on Google. Oh no. They add a ‘spread’ – essentially, they buy the currency from you at a slightly lower rate and sell it to you at a slightly higher rate. That difference is pure profit for them.

- Typical Spread: 0.5% – 3.5% above the mid-market rate. This can easily cost you an extra $50 on a $2,000 transaction!

Withdrawal/Payout Fees (The ‘Getting Your Money Out’ Fee)

Once the money is in your facilitator account, you often need to move it to your actual bank account. Surprise! That can cost you too.

- Typical Range: $0 – $25 per withdrawal, or a percentage (e.g., 0.5% – 1.5%) for larger amounts.

Chargeback Fees (The ‘Customer Changed Their Mind’ Penalty)

If a customer disputes a charge, the facilitator will hit you with a chargeback fee, even if you win the dispute. It’s a penalty for the hassle.

- Typical Range: $15 – $50 per chargeback.

Monthly/Setup Fees (The ‘Just Because’ Fee)

Some platforms, especially those catering to larger businesses, might have monthly maintenance fees or even a setup fee.

- Typical Range: $0 – $100+ per month, $0 – $500+ setup.

Here’s a quick look at how these fees stack up:

| Fee Type | Description | Typical USD Range |

|---|---|---|

| Transaction Fee | Percentage + fixed fee per sale | 1.5% – 4.5% + $0.20-$0.50 |

| Currency Conversion (FX) | Hidden spread on exchange rate | 0.5% – 3.5% of transaction value |

| Withdrawal/Payout | Moving funds to your bank | $0 – $25 per withdrawal or 0.5%-1.5% |

| Chargeback Fee | Penalty for disputed transactions | $15 – $50 per incident |

| Monthly/Setup Fee | Subscription or initial cost | $0 – $100+ monthly, $0 – $500+ setup |

Which are the best payment facilitators cross border transactions 2026?

Alright, let’s get down to brass tacks. For 2026, the players are largely the same, but their features, fees, and focus continue to evolve. Here’s a no-BS comparison:

| Facilitator | Target Business | Transaction Fees (Typical) | FX Rates (Spread) | Payout Speed | Supported Currencies (approx.) |

|---|---|---|---|---|---|

| Stripe | Growth-focused e-commerce, SaaS | 2.9% + $0.30 (domestic), 3.9% + $0.30 (international) | 0.5% – 2% | 2-7 business days | 135+ |

| PayPal (Business) | Small to medium e-commerce, marketplace sellers | 2.9% + $0.30 (domestic), 4.4% + fixed fee (international) | 2.5% – 4.5% | Instant (to PayPal balance), 1-5 days (to bank) | 25+ |

| Wise (formerly TransferWise) | Businesses needing low FX costs, international payouts | 0.43% – 2.5% (variable by currency/amount) | 0.35% – 1% (very competitive) | Same day – 2 business days | 50+ |

| Payoneer | Freelancers, marketplace sellers, global payouts (Asia focus) | 0% (receiving from same Payoneer), 0.5% – 3% (receiving from others), 2% (withdraw to local bank) | 0.5% – 2% | 1-3 business days | 150+ countries (local receiving accounts) |

| Adyen | Large enterprises, omnichannel, global brands | 0.6% – 1.2% + $0.12 (processor fee, varies greatly by payment method) | 0.5% – 2% | 1-3 business days | 150+ |

Stripe: The Developer’s Darling, But Not Just for Techies

Stripe is powerful, flexible, and great for businesses wanting to integrate payments directly into their website or app. It handles almost every payment method under the sun. Their fees are transparent, but the international transaction fees can add up. Good for scaling businesses.

PayPal: The Granddaddy, Still Relevant but Pricey for FX

Everyone knows PayPal. It’s trusted by consumers globally, which is a huge plus for conversion rates. For small businesses just starting international sales, it’s easy to set up. However, their currency conversion rates are notoriously bad. If you’re doing high volume in different currencies, those FX fees will eat your lunch.

Wise (formerly TransferWise): The FX Champion

If your main concern is getting the best possible exchange rate for international transfers, Wise is your go-to. They use the real mid-market rate and charge a small, transparent fee. Excellent for paying international suppliers or receiving payouts in multiple currencies. Not a full-blown payment gateway for your e-commerce store, but brilliant for managing actual money movement.

Payoneer: The Marketplace & Freelancer Friend

Payoneer excels at facilitating payments for marketplace sellers (Amazon, eBay, etc.) and freelancers. They offer local receiving accounts in multiple currencies, which can save you a ton on FX when marketplaces pay you. Their fees for withdrawing to your local bank are competitive. Good for businesses with a strong presence on international platforms.

Adyen: The Enterprise Solution

If you’re a big fish with complex global needs, Adyen is a beast. They offer a unified platform for online, in-app, and in-store payments, with advanced fraud prevention and data analytics. Their pricing is highly customized and generally more favorable for high-volume merchants. Probably overkill for most small to medium e-commerce sellers.

How to choose the right facilitator for YOUR business?

Don’t just pick the cheapest headline fee. That’s a rookie mistake. You need to consider your specific needs.

1. Your Customer Base & Payment Methods

Where are your customers? What payment methods do they prefer? If you’re selling to Germany, SEPA Direct Debit is huge. If it’s China, WeChat Pay and Alipay are kings. Make sure your facilitator supports the local payment methods your customers actually use. If you’re selling a variety of products globally, understanding what we ship and how it impacts payment flows is crucial.

2. Your Volume & Average Transaction Value

Low volume, high value? High volume, low value? The fee structure that works best for one might kill the other. Some facilitators offer better rates for higher volumes.

3. Your Geographic Reach (Where You Sell, Where You Get Paid)

Do you need to receive payments in 5 currencies or 50? Some facilitators are stronger in certain regions or offer more local bank account options.

4. Ease of Integration & Technical Skills

Are you a coding wizard, or do you rely on Shopify apps? Stripe is powerful but needs some technical know-how. PayPal is plug-and-play. Choose what matches your technical comfort level.

5. Payout Speed & Settlement Currency

How quickly do you need access to your funds? Some platforms hold money longer. Also, can they settle directly into your preferred currency, or will you incur another FX fee?

Key Features to Look For (beyond just fees)

- Fraud Prevention: Essential for protecting your business from chargebacks and scams. Look for robust tools like 3D Secure, address verification, and machine learning.

- Reporting & Analytics: Can you easily track transactions, reconcile accounts, and understand your payment data? Good reporting saves you hours of admin.

- Customer Support: When things go wrong (and they will), can you get a human on the phone? In your time zone? In a language you understand?

- Multi-currency Support: Not just accepting, but also holding and settling in multiple currencies.

- Scalability: Can the platform grow with your business? Adding new features, markets, or payment methods should be straightforward.

Avoiding common payment processing pitfalls.

Beyond picking the right facilitator, you need to be smart about how you operate.

1. Don’t Neglect Landed Cost

Your payment processor fees are just one piece of the puzzle. You also have shipping, duties, taxes, and customs. Use a Landed Cost Calculator to get a full picture of your profit margins. If you don’t factor in all costs, you’re just guessing. This is especially critical when considering services like DDP Shipping Service where duties and taxes are prepaid.

2. Understand Local Regulations

Different countries have different rules about payment processing, data privacy (GDPR!), and consumer protection. Make sure your chosen facilitator (and you) comply. Ignorance is not an excuse when regulators come knocking. Our Customs Clearance Guide can give you a head start on understanding some of these complexities.

3. Diversify (If It Makes Sense)

Don’t put all your eggs in one basket. For larger businesses, having a backup payment processor can prevent catastrophic outages. For smaller businesses, it might mean using PayPal for some markets and Stripe for others, or Wise for supplier payments.

4. Negotiate!

If you have significant volume, don’t be afraid to negotiate fees. Especially with Stripe or Adyen, there’s often wiggle room if you can prove your transaction volume.

Future-proofing your payment strategy for 2026 and beyond.

The payment landscape is always changing. Here’s what to keep an eye on:

- Real-time Payments: Instant payment networks are expanding globally. This means faster settlement for you and your customers.

- Alternative Payment Methods: Crypto, ‘Buy Now, Pay Later’ (BNPL), and local digital wallets will continue to grow. Make sure your facilitator can adapt.

- Embedded Finance: Payment processing becoming an almost invisible part of other services.

- AI & Machine Learning: Expect even smarter fraud detection and personalized payment experiences.

The bottom line for e-commerce sellers in 2026 is simple: be smart, be vigilant, and don’t let anyone take a bigger slice of your pie than they deserve. The ‘best’ facilitator isn’t a one-size-fits-all answer; it’s the one that fits your business like a glove, minimizes your costs, and maximizes your peace of mind.

Don’t just guess your total costs when shipping internationally. Factor in all fees, from payments to freight. Use our Landed Cost Calculator to ensure you’re pricing your products right and truly understand your profit margins before you even think about the payment processing side. Knowing your full costs upfront is the only way to succeed in global trade, whether you’re using Air Freight from China or sea cargo.

Frequently Asked Questions

Which is the absolute best cross-border payment facilitator for 2026?

The ‘best’ depends on your business. For low FX fees, Wise is excellent. For broad e-commerce integration, Stripe is strong. For marketplace sellers, Payoneer is great. PayPal is widely accepted but often has higher FX costs. Adyen is for large enterprises.

What are the hidden fees I need to watch out for with cross-border payments?

Look beyond the headline transaction fee. Hidden costs include currency conversion (FX) spreads (often 0.5% – 3.5% of the transaction), withdrawal fees ($0 – $25), and chargeback fees ($15 – $50). Always read the fine print on their pricing page and compare the actual exchange rates they offer versus the mid-market rate.

How do I choose the right payment facilitator for my e-commerce business?

Consider your customer’s location and preferred payment methods, your transaction volume and value, your geographic reach, ease of integration with your e-commerce platform, and payout speed. Also, evaluate their fraud prevention tools and customer support.

Why do I need a payment facilitator instead of just using my regular bank?

A payment facilitator streamlines international money transfers, often offering better exchange rates and lower overall fees than traditional banks. They handle the complexities of cross-border transactions, local payment methods, and compliance, making it easier for you to sell and get paid globally.

What are the major trends in cross-border payments for 2026 and beyond?

For 2026, expect continued growth in real-time payments, diverse alternative payment methods (like crypto and BNPL), and embedded finance solutions. AI and machine learning will also enhance fraud detection and personalize payment experiences. Your chosen facilitator should be able to adapt to these trends.