For UK-bound designer apparel from China, correct tariff classification is the single most critical factor determining border clearance speed and total landed cost. Misassigning a commodity code – even by one digit – can trigger HMRC audits, costly demurrage, and missed retail seasons.

While many importers fixate on freight rates, the true variable lies in the 10-digit commodity code under the UK Global Tariff. This code dictates your exact duty rate, VAT liability, and any supplementary licensing requirements. With the UK operating a fully independent customs regime post-Brexit, EU anti-subsidy measures do not apply – but British classification rules are stringent and unforgiving.

This guide breaks down the essentials: the difference between Chapter 61 (knitted) and Chapter 62 (woven), how to decode the 10-digit structure, and how to accurately value luxury items including royalties. Master these fundamentals to secure predictable customs clearance and protect your margins.

The Divergence Between UK Global Tariff and EU Frameworks

Since the implementation of the post-Brexit trade framework, the UK administers its own independent customs platform known as the UK Global Tariff. Any recent protective tariffs, anti-subsidy penalties, or trade defense measures finalized by the European Union do not apply to goods cleared for home consumption within Great Britain and Northern Ireland. Instead, all apparel shipments from non-preferential nations must conform to the definitive rules set forth by HM Revenue and Customs (HMRC).

Because China does not currently share a bilateral free trade agreement with Britain, all textile imports are subjected to the standard third-country MFN (Most Favored Nation) duty rates listed under the UKGT. While an apparel item destined for France or Germany might trigger complex EU anti-circumvention tracking or specific European Union community metrics, a parallel shipment entering Felixstowe or Heathrow is evaluated strictly on its 10-digit commodity code under the British Customs Declaration Service (CDS). Consequently, logistics managers must treat the UK as a separate fiscal jurisdiction, ensuring their compliance portfolios match British statutes rather than European codes.

Master UK Commodity Codes for Premium Garments

Determining your exact financial liability at the British border requires the assignment of a precise 10-digit commodity code to every stock-keeping unit (SKU) within your shipment. For luxury clothing, classification is notoriously complex, as duties shift based on material composition, gender designation, and the precise construction of the item.

Chapter 61 vs. Chapter 62 Nomenclature

The broader world of apparel classification under the international Harmonized System (HS) is split into two primary chapters. Importers must verify the exact textile manufacturing technique before preparing customs invoices:

- Chapter 61 (Knitted or Crocheted Apparel): This chapter covers items formed by interlocking loops of yarn. It includes high-end knitwear, premium jersey blend shirts, and structured athleisure lines.

- Chapter 62 (Not Knitted or Crocheted Apparel): This chapter governs woven garments where yarns cross at right angles. This applies to traditional designer suits, evening gowns, tailored trench coats, and denim luxury lines.

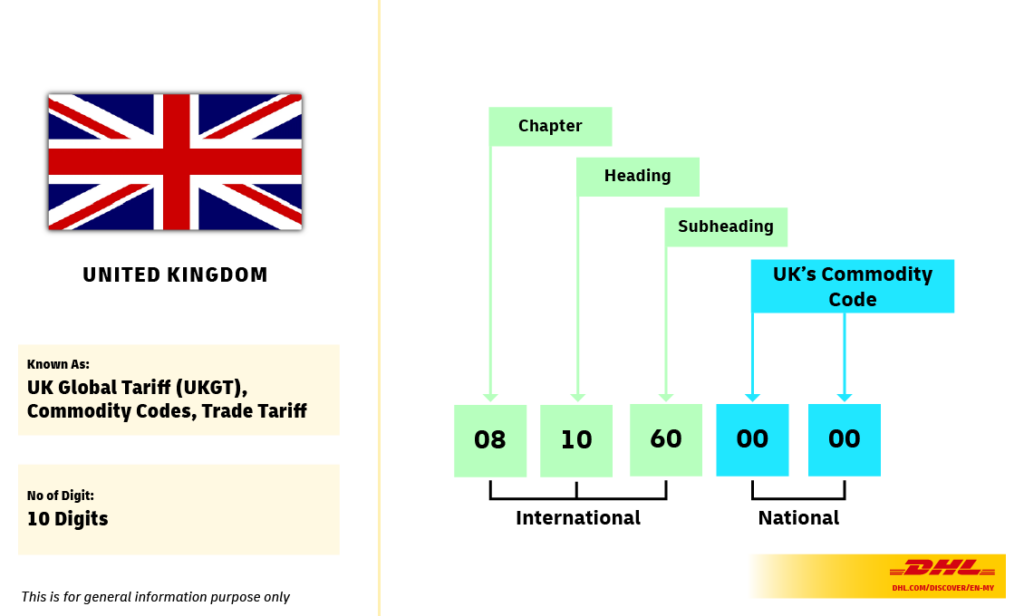

Deconstructing the 10-Digit Code Structure

While the first 6 digits of an apparel code are standardized globally under the World Customs Organization (WCO) nomenclature, the remaining 4 digits are completely unique to the British trade system. When importing designer apparel from China to the UK, the full 10-digit sequence dictates your precise border treatment. The code structure behaves as an administrative funnel:

- Digits 1–2 (Chapter): Specifies the broad textile category (e.g., Chapter 62 for woven apparel).

- Digits 3–4 (Heading): Refines the garment type (e.g., Heading 6204 for women’s woven suits, jackets, and dresses).

- Digits 5–6 (Subheading): Details the explicit product design style (e.g., trousers versus skirts).

- Digits 7–8 (UK Tariff Heading): Determines the material category, distinguishing between pure silk, wool, fine animal hair, synthetic fibers, or cotton blends.

- Digits 9–10 (TARIC/National Measures): Dictates the precise UK Global Tariff duty rate, VAT thresholds, and any active trade licensing restrictions enforced at the port of entry.

Technical Comparison Matrix: Material Classifications and Duty Rates

The following data table illustrates how variations in a garment’s physical composition directly alter the customs valuation and duty liabilities under standard UKGT rules.

| Garment Type (Woven) | 10-Digit UK Commodity Code | Primary Material Composition | UK Global Tariff Duty Rate | Import VAT Rate |

| Men’s Designer Overcoats | 6201 20 00 00 | 100% Woven Wool / Fine Hair | 12.0% ad valorem | 20% |

| Women’s Luxury Blouses | 6206 10 00 00 | 100% Pure Mulberry Silk | 12.0% ad valorem | 20% |

| Premium Evening Dresses | 6204 43 00 00 | Synthetic Monofilament Blends | 12.0% ad valorem | 20% |

| Designer Denim Trousers | 6204 62 31 00 | Cotton Denim (>240g/m²) | 12.0% ad valorem | 20% |

Mitigating Valuation Risks for High-End Fashion Shipments

Because luxury garments command a substantial premium over mass-produced fast fashion, HMRC targeted audits heavily scrutinize the declared transaction value of designer cargo. Importers must execute strict administrative safeguards to prevent catastrophic non-compliance flags.

Establishing Verifiable Valuation Methods

Customs duty is calculated on a CIF (Cost, Insurance, and Freight) basis. This means the 12% duty rate is applied to the combined value of the physical garments, the marine cargo insurance policy, and the total ocean or air freight costs required to bring the container to the UK border. Importers must utilize Method 1 (Transaction Value) backed by verifiable proof of payment, such as bank swift confirmations matching the exact commercial invoice total. Under-declaring the value of designer clothing to evade the standard 12% UK Global Tariff duty triggers immediate asset forfeiture, severe financial penalties, and the revocation of your corporate deferment account.

Managing Royalties and Licensing Fees

A major pitfall unique to the designer apparel classification space involves the treatment of intellectual property rights. If your UK entity pays a separate royalty, trademark fee, or licensing license to a brand house or design studio as a condition of sale for the imported items, this fee must be legally declared and added to the customs value. Failure to include these auxiliary payments on your CDS declaration forms constitutes a structural misdeclaration, exposing your business to retrospective tax assessments covering up to three years of historical imports.

Summary: Securing Your Fashion Supply Chain

In summary, successful textile importation relies on a proactive approach to customs compliance. By recognizing that UK borders are entirely independent of EU trade decisions, identifying the exact material breakdowns across Chapters 61 and 62, and calculating duties using verified CIF valuations, premium fashion brands can secure continuous customs clearance. Investing in precise data classification is the definitive mechanism to insulate your retail operation from unexpected operational disruptions and secure stable fiscal management.

Internal Linking Network

To further refine your international logistics strategies and mitigate financial border exposure, explore our technical operational briefs:

- Evaluate your cost optimization strategies by reviewing our detailed guide comparing China freight forwarders versus local port clearing brokers.

- Ensure your valuation mechanics satisfy regional compliance mandates by examining our technical breakdown on UK HMRC customs valuation rules for premium apparel.

- Protect your capital assets against maritime transit damage risks by setting up cargo insurance protocols for cross-border DDP freight.

Download the 2026 Customs Compliance Blueprint

If you need to verify that your active clothing shipments match the exact statutory demands of HM Revenue and Customs, download our automated classification vetting tool.

Receive an actionable, technical compliance PDF containing detailed classification checklists, step-by-step guidance on calculating luxury royalty additions, and exact documentation templates to prepare your designer inventory for intensive border inspections.

Frequently Asked Questions

Can a fashion brand rely on generic sustainability certificates for customs clearance?

No. While global sustainability frameworks are excellent for brand marketing, the UK Border Force does not accept them as primary legal evidence of origin compliance. Customs authorities require factual, unlinked transactional documents, such as commercial invoices, shipping manifests, and specific raw material purchase logs that physically tie back to the specific batch being imported.

What happens to my freight costs if a clothing shipment is detained for tracking audits?

When a container is issued a formal detention notice, the importer is legally liable for all terminal storage, drayage, and container devanning fees accrued during the audit window. These costs pass through to your account and can quickly exceed thousands of pounds if your logistics operator lacks a dedicated compliance team to resolve the documentation hold quickly.

How does a cross-border freight forwarder verify textile compliance before shipping?

Professional logistics providers run automated document audits at their origin warehouses in China. Shippers must present their material safety data, bills of lading, and verified supplier declarations before the goods are cleared for container consolidation, ensuring that no non-compliant or unvetted textile freight enters the shared transport stream.